There have been numerous discussions on the benefits of rounding cash transactions due to the fact that the penny has minimal buying power for consumers and the penny production costs to the U.S. Mint have exceeded the face value of the coin for some time. This article attempts to clarify the impact of rounding on retailers using the well documented practices summarized below.

For most retailers, a key component of penny costs includes the delivery of pennies to retail stores. Isolating the penny portion of the costs is challenging as “coin” is part of a larger “change order” consisting of numerous coin denominations and banknotes which are typically delivered in conjunction with a commercial deposit pick-up. Isolating the penny costs may be difficult but retailers can identify “coin” costs as the majority of depository institutions clearly specify a “coin roll” or wrap rate.

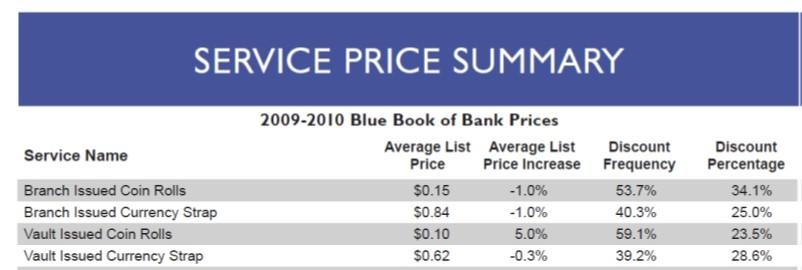

Phoenix and Hecht previously published the Blue Book of Bank Prices which identified the Average List Price, Price Increases, Discount Frequency and Percentages for many bank services. The Blue Book is no longer published but the final edition, which was published in the 2009-2010 timeframe, identified the following rates for coin rolls which we will use for this analysis.

The adjacent table uses the vault issued rate of $.10 from the above. Discount percentages vary by retail customer due to overall volumes. Line item 2 identifies potential discounts; the estimated per roll costs (line 4) are used to estimate rounding costs vs. penny usage below.

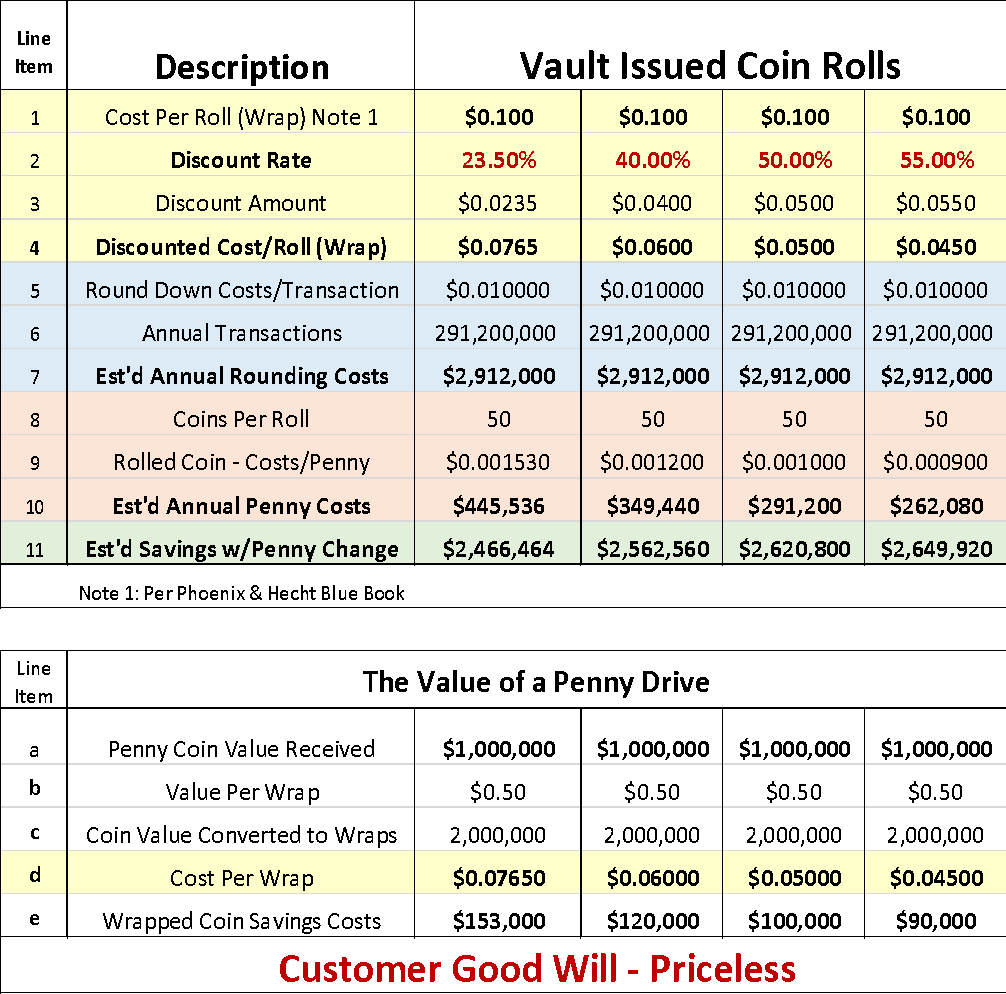

The FDIC identifies 5.6M unbanked U.S. households; one weekly cash purchase per household generates 191.2M cash transactions yearly.

The costs to the retail sector for each penny rounded in favor of the customer may cost the sector $2.45M+ annually, rounding 2¢ per cash transaction may costs retailers more than $4.9M annually, etc.

The costs to acquire a penny in a coin roll is $.001530 (line 8 & 9), the difference between one penny for change and the costs for rounding calculated as $.01 minus $.001530 = $0.008470, revealing that it costs less to acquire a penny to provide the correct change than it costs to round down – revealing very real rounding costs for the retail sector.

The retailers that have posted signs requesting exact change on cash purchases or the use of another payment method would seem to be unconcerned about rounding, electing to pay card fees on the value of the entire transaction vs. incurring penny roll or rounding costs.

As revealed above the penny may have minimal consumer buying power, but it may be vital for many retailers for change funds.

The analysis above is also useful to estimate the benefit of the penny redemption drives/offers conducted by some retail stores.

For example, the Giant Eagle Stores revealed that they collected $1M in pennies during their recent penny drive. The coin will need to be managed at the store level but recycling coin redeemed from consumers back to other consumers at the retail store is undoubtedly very efficient and dependent on the roll rate (line 4 above) the supply of 2-million-coin rolls may have reduced the costs for rolled coin to Giant Eagle by $90,000 to $153,000 as indicated on (line item “e”) on the lower table above.

Additionally, anecdotal evidence revealed that the recent penny drive conducted by the Price Chopper / Tops branded stores in the Pennsylvania and New York markets attracted individuals that did not typically deposit their loose or otherwise idle coin.

Could future penny or general coin drives re-introduce significant coin supplies into the U.S. circulating coin inventory to thus potentially offset the reduction in penny supplies as a result of the U.S. Mint no longer manufacturing pennies?

.svg)

.jpg)